This is the second article in a two part series comparing the Q3 2022 performance numbers of Bitfarms (BITF), Hive Blockchain (HIVE), Hut 8 (HUT), Marathon Digital (MARA) and Riot Blockchain (RIOT). This article covers the Bitcoin mining costs per company, year-to-date production costs by EH/s and balance sheet fundamentals.

Read: Ranking the top five Bitcoin miners: Part I

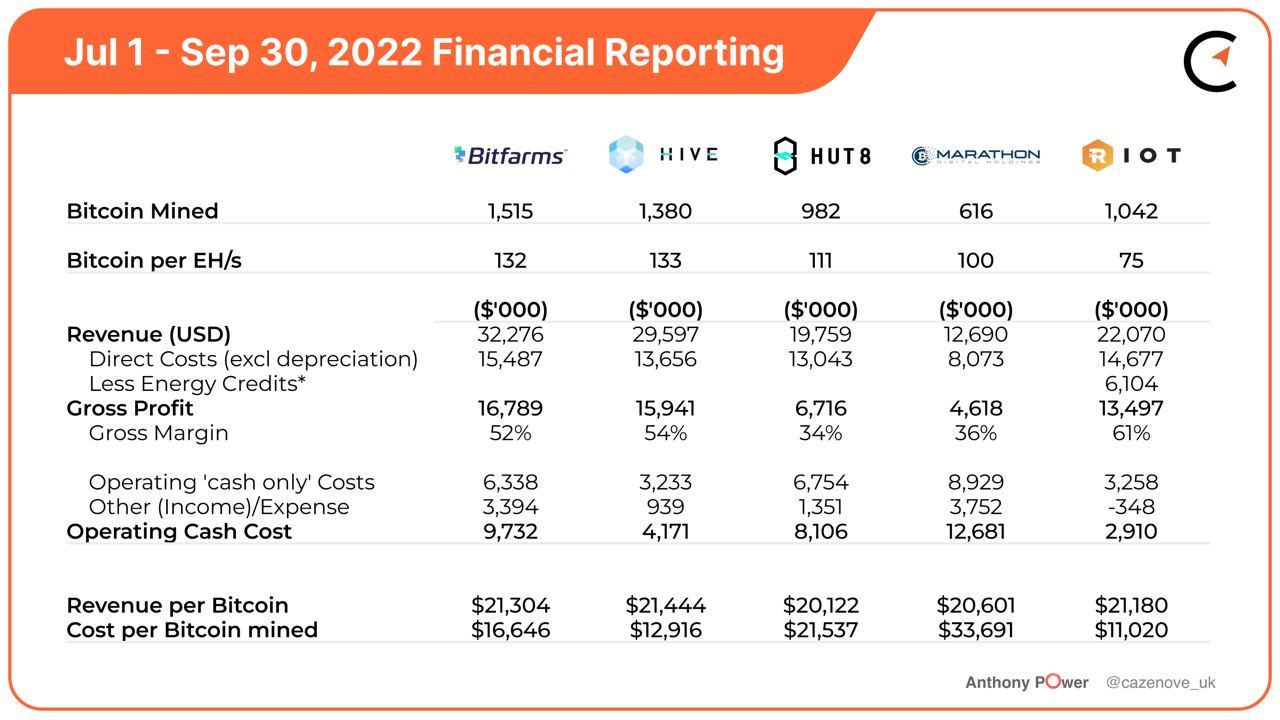

The cost of mining a Bitcoin is fundamental to any miner analysis. Over Q3, profit margins began to squeeze even further as Bitcoin’s price remained deflated and difficulty began to creep upwards. Of the miners surveyed, Riot Blockchain produced the cheapest Bitcoin at an all-in cash price of $11,020 per coin with Hive Blockchain a little higher at $12,916 per coin.

- Hive Blockchain and Bitfarms managed to maintain 54% and 52% margins, respectively.

- Riot Blockchain although having to apply a significant amount of curtailment has effectively achieved a gross margin of 61%. This figure actually includes $6.1 million of the total $13.1 million energy credits received in the quarter, attributed to self mining.

- Hut 8 and Marathon Digital both had margins of 34% and 36%, respectively. However, they effectively paid more during the period to mine Bitcoin than revenue generated.

(Physical ‘cash costs’ are taken from the recent quarterly reportings, while non-cash items such as depreciation, stock compensation and impairment charges are ignored. I have also utilized segmental reporting where miners are producing revenues and costs for services other than self-mining. The gross mining profit predominantly takes into account the energy cost of mining and is therefore a useful comparator for mining operations that are effectively occurring in different continents).

With the current price of Bitcoin currently around $17,000 per coin, over $3,000 (15%) less than the reporting period, it's going to be a challenging time for many Bitcoin miners, particularly Hut 8 and Marathon Digital, to keep their physical cash costs within this figure.

YTD Bitcoin production by EH/s

- Hive Blockchain has been the most consistent miner over the past ten months, closely followed by Bitfarms, who themselves have actually been top monthly producer in no less than seven of the calendar months this year.

- Riot Blockchain’s production has been affected by curtailment for most of the year, but they’ve used this to its advantage by selling blocks of energy back to the grid when prices spike.

- Marathon Digital had a poor first 6 months in terms of production, already well documented, but they appear to be moving in the right direction with an increased operational hash rate of 7.0 EH/s and good mining results in October.

- Hut 8 has been a steady performer throughout the year but it will be interesting to understand how the current dispute with Validus Power, its energy provider at the North Bay facility in Ontario, where 5,800 miner rigs are currently plugged in, will conclude.

Balance sheet fundamentals

A miner is only as strong as its balance sheet allows. Here, we look at a few metrics to better understand public miners positions based on their equity marketcap, assets, liabilities and so on.

The first metric, the current ratio, also known as the liquidity ratio, measures a company’s ability to pay short-term obligations or those due within one year. It provides investors and analysts the ability to interpret how a company can maximize the current assets on its balance sheet to satisfy its current debt and other payables by the current assets, i.e. those assets that can be liquidated into cash within the next 12 months.

Hut 8 has a very positive ratio and can cover its current liabilities by a factor greater than nine. On initial analysis, Marathon Digital looks to have reasonable liquidity levels, but they currently have two loans totalling $100 million leveraged by Bitcoin. As the value of Bitcoin has been dropping since the last quarterly update, more Bitcoin will become leveraged and therefore restricted in its use.

As highlighted in the first article, Bitfarms debt levels are higher than many other miners, but they are currently making strides to reduce the levels which should help to improve their balance sheet position.

Hut 8 has a significantly lower Enterprise Value (EV)–a metric that defines an amount which represents the entire cost of the company in case some investor intends to acquire 100% of it–than marketcap, a positive indicator. Marathon Digital has over $800 million of debt on the balance sheet and has an Enterprise Value of $1.47 billion, significantly higher than its market capitalization of $726 million.