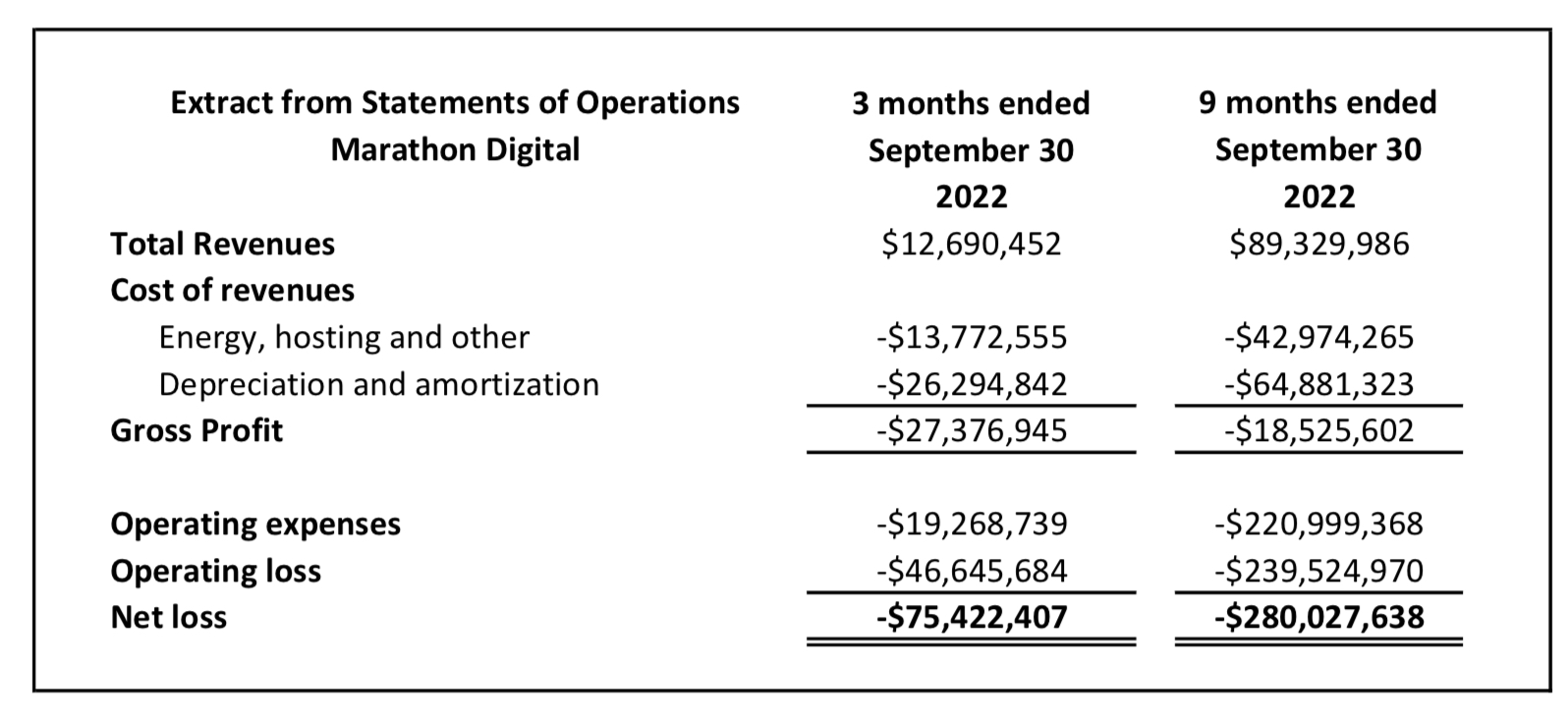

Marathon Digital, one of the largest North American Bitcoin miners listed on the Nasdaq exchange, swung and missed on its reported Q3 financials earlier this month, announcing a $75 million loss during the last financial quarter and a $280 million loss, year to date.

While large, the values are not unexpected, especially when considering Marathon Digital remains one of the largest Bitcoin hodlers of any public company, and the price of Bitcoin has dropped by 75% from its 52-week high. (GAAP accounting standards currently require the impairment of digital currencies held to be recorded. Marathon Digital accounted for a $153 million loss in value, year-to-date).

Yet headwinds persist. Marathon Digital shareholders did not approve the increase in authorized share capital to 300 million at the annual shareholders meeting on Nov. 4. This decision, while understandable in the current climate, could negatively impact the firm’s ability to keep pace with competitors. For example, Riot Blockchain’s shareholders approved a similar measure to increase the number of issued shares in May 2022, allowing for aggressive infrastructure developments.

Gross mining profit–when taking the revenue and deducting the direct costs associated with mining–were only 36% over the last three months. Margins are getting squeezed when you consider the company was achieving over 80% margins earlier in the year, leaving less to meet their operating obligations, like salaries, professional fees and interest repayments.

Lastly, Marathon Digital has not currently sold any of its 11,440 Bitcoin held, but 83% are held as leverage against two loans totaling $100 million. They may face capital calls as a result of these loan agreements, which could lead to the company having insufficient capital to cover the calls and therefore force Marathon Digital to consider options of reorganization or liquidation.

In this article, we will take a look at some defining moments Marathon Digital faced this past year, a survey of its debt obligations and conclude with a note on its Bitcoin production.

Key challenges

- Hardin, Montana, exit: The company completed the exit from the Hardin facility in September, selling 22,000 of the 30,000 mining servers deployed there for cash proceeds of $46.5 million. The acceleration out of Hardin also meant the company taking a larger amortization and depreciation charge of $15.1 million plus additional costs of $5.7 million, which are both reflected in the company’s direct costs.

- Compute North: Marathon Digital’s main hosting provider, Compute North, filed for Chapter 11 bankruptcy on Sept. 22. The company has assessed the impairment of these assets and recorded an impairment charge of $39 million as of Sept. 30, reducing the overall exposure to Compute North to approximately $42 million, primarily in deposits associated with King Mountain and Wolf Hollow. The full recoverability of these deposits remains a risk given the ongoing bankruptcy proceedings.

- Legal Reserves: Marathon Digital agreed to a settlement of certain restricted stock unit awards previously granted to the former Chief Executive Officer and Chairman for a total of $24 million. Marathon Digital also entered into related settlement agreements, totaling $1 million in respect to five other recipients of the same restricted stock unit awards, including Fred Thiel, a director and current Chief Executive Officer and Chairman.

- Stock compensation: Stock compensation has dropped for the first nine months of 2022 to $18.9 million from a total of $152.3 million in the same period during 2021. The compensation is tied to the company achieving its future planned hashrate of 23 EH/s. It would be fair to assume that senior management will receive an element of the stock compensation at various hashrate levels up to their target.

- EBITDA and adjusted EBITDA: Although not a requirement of GAAP, many of the listed Bitcoin miners also report EBITDA, which takes Earnings and adds back interest expenses, taxes, depreciation and amortization charges. They also apply other generally one-off adjustments to provide an adjusted EBITDA.

The table below highlights the reconciliation from net loss to adjusted EBITDA.

Debt levels

Many a strong miner became too intoxicated with debt during the bull market, ultimately becoming its undoing during the eventual drawdown. As such, every miner requires scrutiny to understand where its financial health stands. For Marathon Digital, three lines of finance are of importance: a convertible senior note issued at 1.0% in November 2021, a $100 million term loan, and a revolving credit line (RLOC) of $100 million, both loans with Silvergate Bank.

For context, on Nov. 18, 2021–when the miner’s market capitalization was close to $5.5 billion–the company issued $650 million principal amount of its 1.00% convertible senior notes. An option was exercised on Nov. 23, 2021, to increase this by an additional $97.5 million. These notes will mature on Dec. 1, 2026, and noteholders will have the opportunity with effect from June 1, 2026, until the maturity date to convert their notes into cash or shares in the company or a combination of both. At today's share price of $6.19, Marathon Digital has a market capitalization of $723 million, a drop of 87% since the notes were issued.

To date, the company has borrowed $50 million of the term loan, which carries a variable interest rate of prime rate plus 1.75%, (8.75% at today's market rate). The RLOC includes the opportunity for the company to borrow up to $50 million more, within 270 days after closing the initial $50 million. During October 2022, Marathon Digital exercised a further $50 million loan under the RLOC facility, providing 3,993 Bitcoin as collateral. Marathon has also used the RLOC facility to pay down the term loan without penalty.

The total collateral balance for the two loans, totalling $100 million, at this point was 7,821 Bitcoin. However, with the value of Bitcoin falling to $16,212, the company has had to issue an additional 1,669 Bitcoin, taking the total collateral balance to 9,490 Bitcoin to cover the loans.

As of now, the annual interest payments on these loans and notes is currently in excess of $15 million. The amount of unrestricted Bitcoin held by Marathon Digital is now 1,950. More collateral will be required if Bitcoin’s price continues to draw down. If the Bitcoin price was to drop lower than $13,500, there would be insufficient collateral to cover these loans. In other words, watch for a possible restructuring of these loans if Marathon or Silvergate think it's in their best interests to do so.

2022 Bitcoin Production

Q3 2022 was a rebuilding phase for Marathon Digital, beginning with the closure of Hardin and ending with miners going online at Compute North’s former facility.

Producing 616 Bitcoin during the quarter, Marathon actually recorded a monthly production in October 2022 of 615 Bitcoin with 7.0 EH/s online. Still, Marathon would need to produce 40% more Bitcoin to produce similar levels of Bitcoin per EH/s online posted by peer miners Hive Blockchain (HIVE), Iris Energy (IREN), Bitfarms (BITF) or CleanSpark (CLSK). They are currently forecasting a growth in hashrate to 9.0 EH/s by the end of the year with a current target of 23 EH/s by mid-2023.

In the current financial climate, cash flow is king. A company has to have sufficient cash flow to meet the physical bills of the organization, for example paying for the energy usage, staff and management salaries, site costs, professional fees, interest payments and machine orders.

Marathon Digital will likely continue to need both Bitcoin’s price to rebound and more hashrate to come online quickly in order to meet debt obligations. Marathon Digital may be edging closer to a similar fate as Argo Blockchain (ARB.L, ARBK) and Core Scientific (CORZ), both reporting significant cash flow issues before alerting the markets of possible insolvency. The downtrend in the price of Bitcoin is not helping any of the miners, and only the strongest balance sheets will survive.