Quick take;

- Publicly-listed firms like Square and MicroStrategy gaining exposure to Bitcoin is an extremely bullish demand-side development and may blaze the trail for more publicly-listed firms to enter

- With regulatory approval taking roughly six months for MicroStrategy to buy Bitcoin, other firms may not be ready to deploy capital until Q1 and Q2 of 2021

- United States publicly-listed firms control a significant pool of capital with their combined market capitalization being $36 trillion at the end of September

- $36.7 billion worth of Bitcoin was traded between the demand-side and supply-side over the past quarter

This is the inaugural article of our Bitcoin market analysis series. In this series, we will regularly analyse how Bitcoin fits into the wider macroeconomic picture while attempting to gauge the short-term and mid-term price prospects for the asset.

In the longer-term, one of the most bullish arguments for Bitcoin is its tightening supply schedule. This supply schedule – which hopefully remains secured by the over 6 GW of SHA256 computing power distributed worldwide – means that demand-side players are dominantly forced to purchase from existing holders.

Current holders are showing little propensity to sell while more sophisticated investors enter the market with gigantic purchases. This means that these demand-side players are forced to turn to a small circulating supply which naturally makes the case for upside price movements when demand exceeds supply.

In this market analysis, we highlight how the recent purchases by Square and MicroStrategy may spur other US firms to enter the market. Publicly-listed firms strive to be conventional and the case to buy Bitcoin becomes far more straightforward after an initial risk-taker has taken the leap.

Bitcoin Demand-Side Strengthens as Public Firms Get Exposure

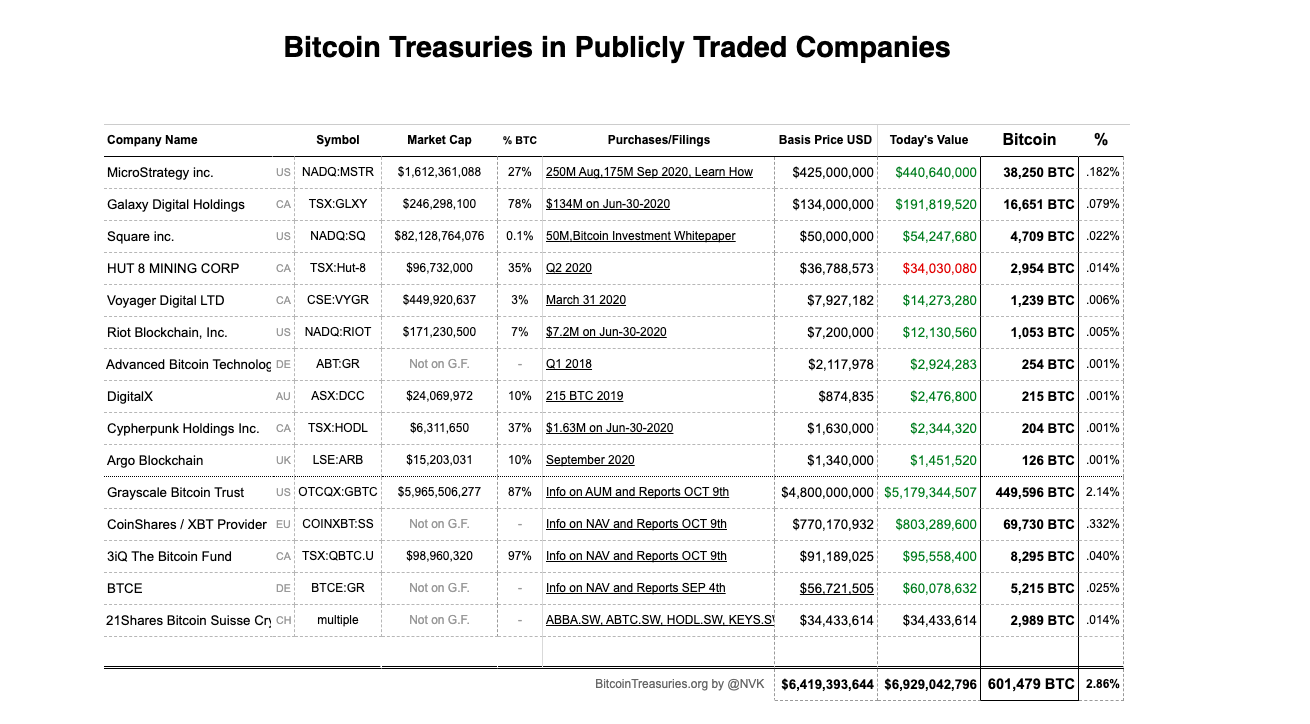

The significant purchases from public firms MicroStrategy and Square Inc is likely the most bullish event of 2020. These firms collectively bought $475 million worth of Bitcoin in recent months. Many are anticipating that this will blaze the trail for more publicly-listed firms to enter the Bitcoin market.

It’s important to note that publicly listed firms need to gain approval from their board of directors if they wish to act on a potentially contentious decision. They are also forced to jump through several regulatory hoops and communicate clearly with shareholders.

Microstrategy CEO Michael Saylor noted that it took the firm roughly six months to gain approval for the significant purchase of Bitcoin. The firm had roughly $0.5 billion worth of cash sitting on their balance sheet and decided to invest the dominant share of that into Bitcoin as an asset allocation strategy.

By nature, publicly-listed firms are risk averse as they’re accountable to the public. But with MicroStrategy being the first publicly-listed firm to buy Bitcoin as part of an asset allocation strategy, others can follow with much more ease as they will not be the first taking this risk.

Firms now starting the approval process may not be ready to deploy capital until Q1 and Q2 of 2021. If the MicroStrategy Bitcoin purchase does catalyze more Bitcoin buying from public US firms, there is a monstrous pool of capital controlled by these corporations. To give a gauge of the size of these firms, the market cap of US publicly-listed firms was estimated to $36 trillion at the end of September.

Bitcoin Supply-Side – Record Long-Term Holding

MicroStrategy and Square pumping $475 million into Bitcoin but this means little without supply context. We have previously highlighted that comparing demand-side to newly issued Bitcoin is futile given that the dominant share of demand-side will be sourced from existing holders.

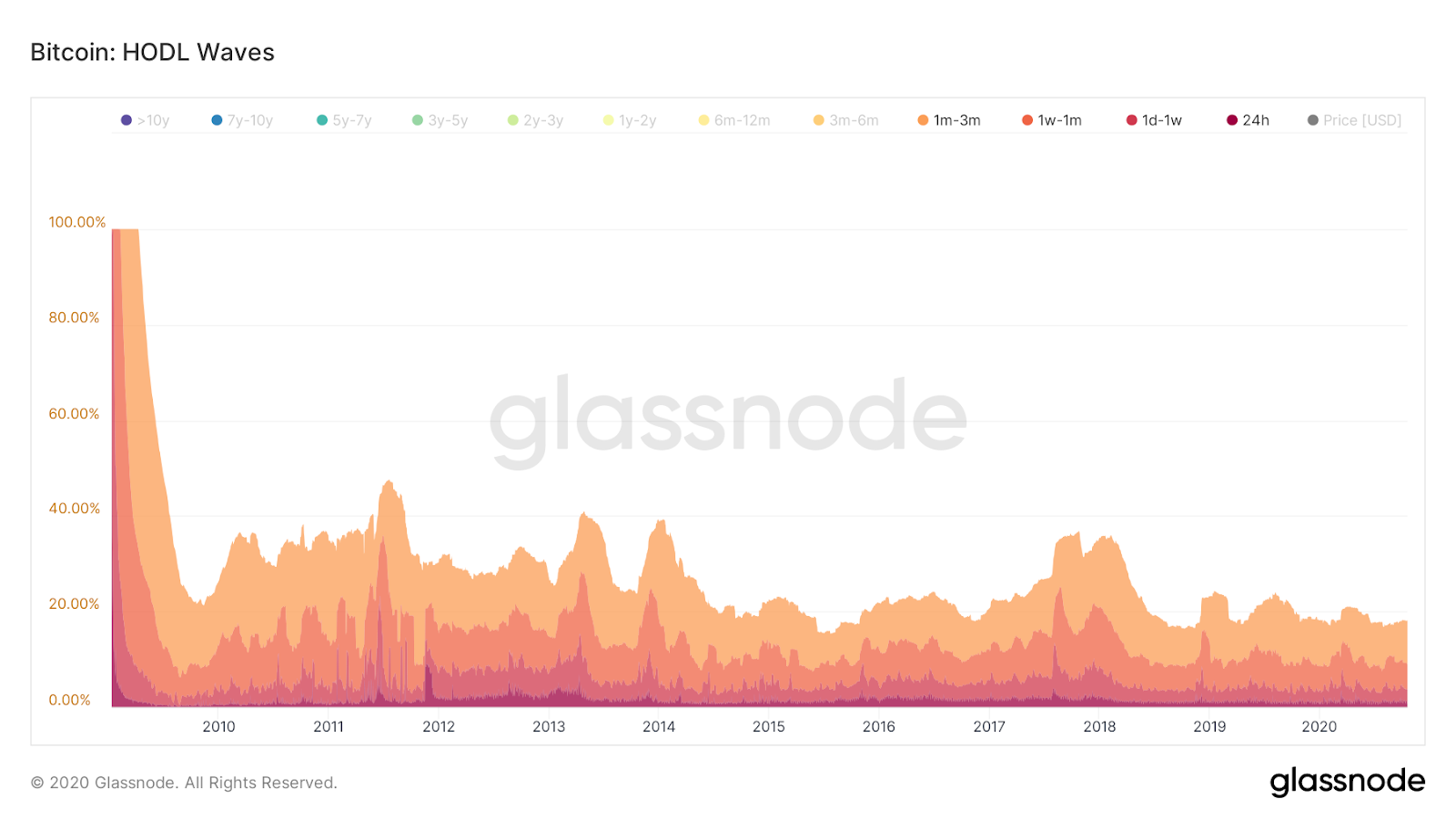

We can gauge how much Bitcoin is moved by existing holders over a quarter by analyzing the Bitcoin UTXO distribution. As it stands, roughly 18% of the circulating Bitcoin supply was moved within the past three months.

To get a gauge of the USD value of Bitcoin moved over the last quarter, we can multiply how much BTC was moved by the 90-day moving average of price. With 18% of the circulating supply representing roughly 3.33 million BTC and the 90-day moving average of price being ~$11,050, approximately $36.7 billion was traded between the demand-side and supply-side over the last quarter.

When the $475 million bought by Square and MicroStrategy is put into this context, it looks far less impressive. It nonetheless represents ~1.3% of the value transferred over the past three months. It also needs to be noted that Bitcoin services other significant markets like exchange inflows and outflows, cross-border payments, and P2P payments. It is easy to make the case that the arrival of some more significant demand-side players making similar purchases to Square and Microstrategy could put considerable upside pressure on price.

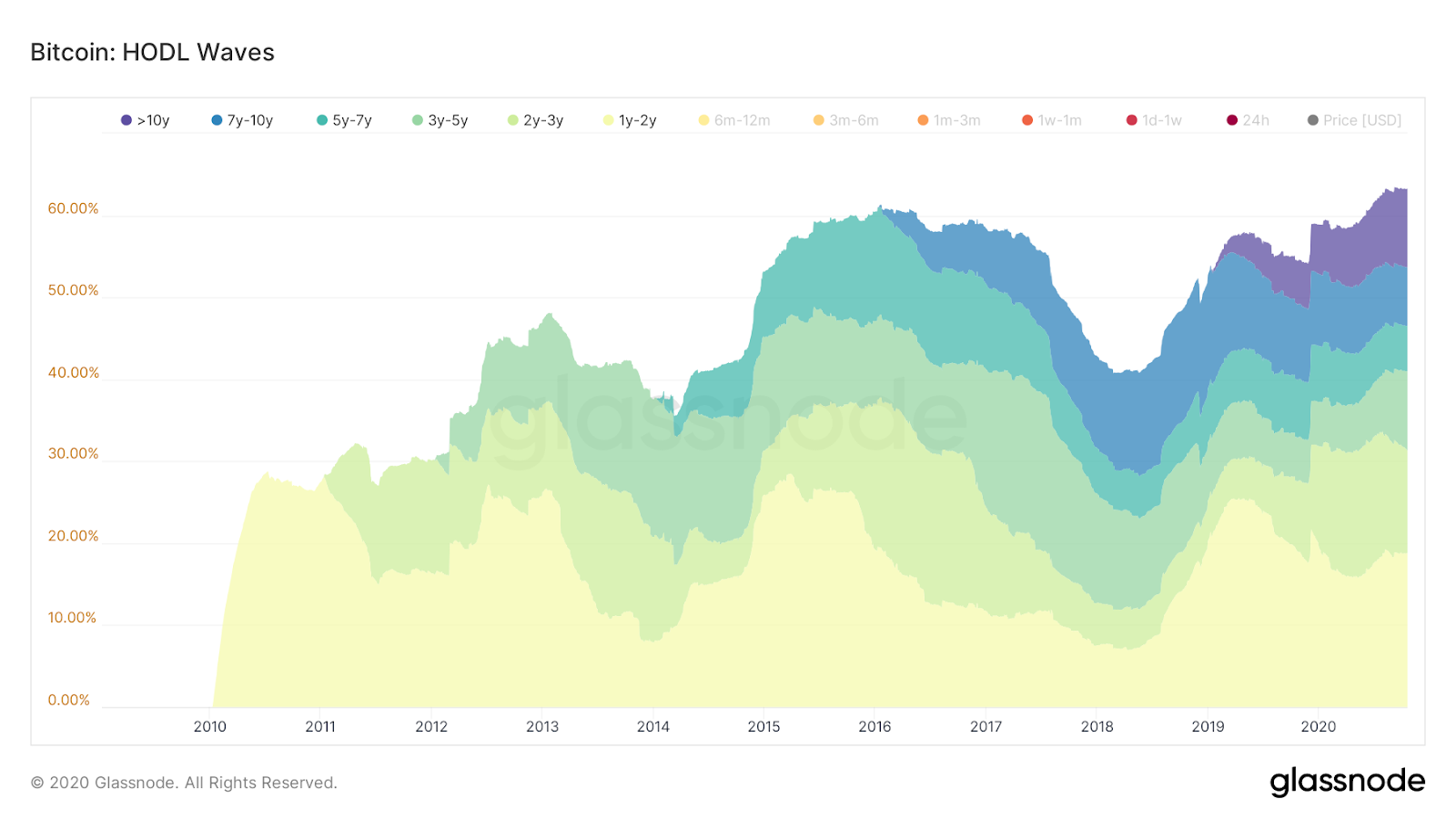

It is also worth noting that long-term holding of Bitcoin is at record levels. Long-term holders are showing a lower propensity than ever to sell their BTC. Bitcoin holders whose BTC is unmoved for 1+ years currently represent 63% of the current circulating supply.

Similar levels were observed in 2016 but this sharply dropped when prices rose in 2017. The percentage of 1+ year holders is naturally expected to decline when prices significantly rise as holders have more incentive to sell their Bitcoin.

The record long-term holdings levels are favourable for upside price movements in Bitcoin. With less holders willing to sell their Bitcoin, demand-side players are forced to source BTC from a constricted supply which will force upside price movements if supply is not sufficient to fulfill demand.

The Tipping Point of Conventionality

While MicroStrategy and Square may only represent a small portion of the Bitcoin traded over the past quarter, the investments made by these firms is likely the most bullish Bitcoin development in 2020. The asset allocations made by these firms reduces the friction for other US public firms to enter the market.

Making a case to invest in Bitcoin as a public firm is now much more straightforward given that other firms have already allocated. It is still a difficult case to make but it nonetheless is more feasible given MicroStrategy’s investment. If the investment goes belly-up, other firms can point to MicroStrategy as the reckless firm that spurred others to enter.

On the flip side of the coin, there may come a point where so many firms gain exposure to Bitcoin that it becomes a bigger risk to not invest. These risk-averse firms strive to be conventional and if most other firms have allocations, they can't risk looking stupid by not having a similar allocation. With the combined market cap of these firms being over $36 trillion, a tipping point occurring would undoubtedly have a monumental impact on Bitcoin’s price.

The 10x-20x price appreciation observed in 2017 was driven by a mass entry of retail capital. A mass entry of US public firm capital would be an entirely different story.